Fundraising

Don’t be fooled by the discount and cap in a convertible loan

29 October 2024

The convertible loan can be a highly effective financial instrument for startups, in that it removes the need to value a startup and bring in an investor immediately as a shareholder.

The historical shareholders (including the founders) and the company should take care to include in the convertible loan agreement the elements common to all loans, such as the amount of the loan, the interest rate, the repayment terms, etc.

In addition to these elements, which are linked to any loan, they will be particularly vigilant regarding the specific elements organising the conversion of the loan and the specific requirements of the investors.

In this respect, we draw your attention to the clauses organizing the discount and the maximum valuation (cap). These two important elements will affect the reference value of the company that will be used for the conversion of the loan and therefore the number of new shares that will be allocated to the investor.

These clauses can have a substantial impact on the dilutive effect of the investment at the time of conversion and therefore on the ‘cost in terms of shareholding’ of the conversion for the historical shareholders. The lower the reference value of the company, the more new shares the investor will receive in the company in return for the contribution of the debt relating to the loan and the more the participation of the historical shareholders will be reduced in relative terms.

The discount – the reward for investing before the others

The lender will generally receive a discount on the reference value of the company used for conversion.

The reference value of the company generally used for the conversion of the loan depends on the circumstances leading up to the conversion. If the triggering event is reaching the maturity date, the price per share is often determined on the basis of the market value set by a third-party expert or, if possible, using a predetermined formula. If the triggering event is a major financing event or an exit, the share price used will be the share price applicable for the financing event or exit (See our article “Convertible loans – How will the loan be converted?”).

This discount represents a profit for the lender due to the additional risk it has taken on by investing in the startup prior to the occurrence of the triggering event determining the reference value. This risk varies according to the circumstances of each situation and is difficult to quantify.

The discount may be fixed or evolve over time. In practice, in Belgium, the fixed discounts usually vary between 20% and 30%. If the conversion of the loan is expected to take place soon after it has been taken out, typically for convertible loans taken out pending the forthcoming completion of a venture capital investment (known as a bridge), we generally recommend providing for a lower percentage that evolves over time.

The cap – the maximum valuation risk that the investor accepts

The parties may agree on a cap, i.e. a maximum valuation of the company for the conversion of the loan into shares.

This is a favourable mechanism for the investor, protecting him against a price per share that would be excessively high at the time of conversion, despite the application of the discount. Generally speaking, investors want to protect their investment against the startup becoming too successful, leading to a sharp rise in its valuation before their investment will be converted. It therefore corresponds to the minimum stake that the investor intends to receive at the time of conversion. Some investors tend to demand a limited cap that corresponds to their idea of the company’s valuation at the time of investment. At Beyond, we do not believe that this corresponds to the philosophy of such a clause.

In contrast to the valuation cap, the parties rarely stipulate a minimum valuation (floor) for calculating the price of the shares when the loan is converted into shares. Unlike the cap, this is a form of protection favourable to the historical shareholders.

It is important to specify that the cap/floor valuation must be applied after the discount has been applied.

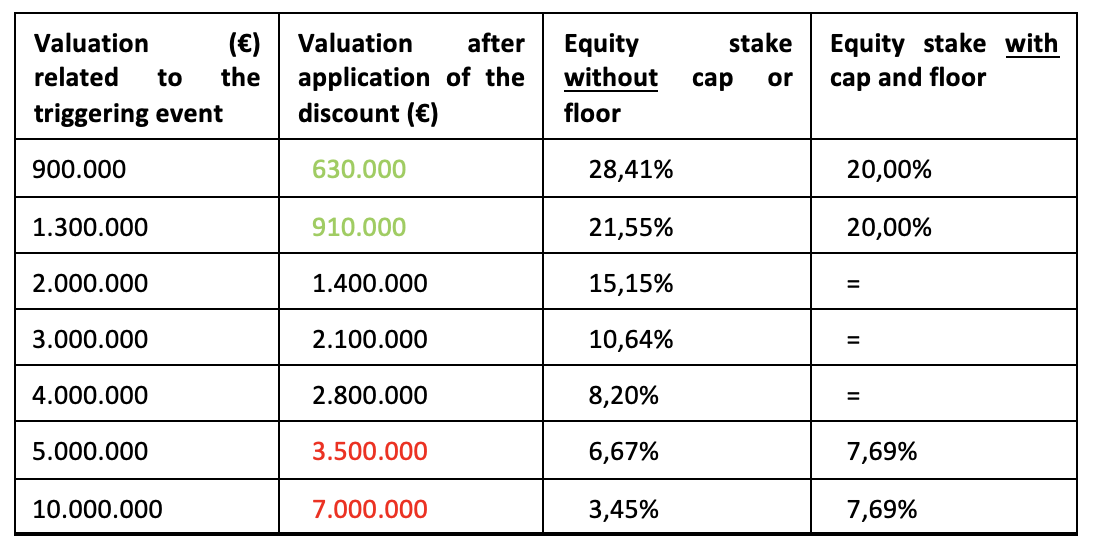

The discount, the cap and the floor in numbers

The following examples illustrate the impact of a cap/floor:

– Investment : 250 000 €

– Discount : 30%

– Valuation cap of 3.000.000 EUR and valuation floor of 1.000.000 EUR (after application of the discount)

Specializing in tech and digital, Beyond Law Firm assists innovative companies with their legal affairs.

Let's talk